The Who and How of Hedge Fund Risk Shifting

Published: October 30, 2024

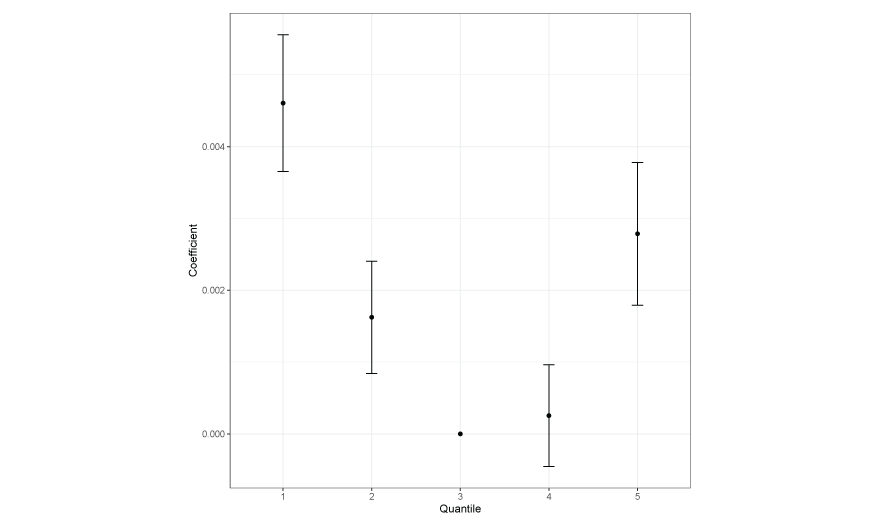

This paper studies whether performance-based compensation incentives influence a hedge fund manager’s investment strategy and the associated risk. Using supervisory data, the authors find that a fund’s relative and absolute performance influence a manager’s behavior and the future risks they take. The analysis considers how hedge fund characteristics like redemption policies and ownership structure affect the way managers respond to underperformance and how their investment strategies can amplify portfolio volatility as they attempt to achieve higher returns (Working Paper no. 24-07).

Abstract

Given the emergence of hedge funds as large intermediaries whose risk-taking affects financial markets, we investigate whether compensation incentives distort the risk choices of fund managers. Using confidential supervisory data on hedge fund returns and characteristics, we fnd strong evidence of risk-shifting behavior consistent with managers attempting to meet performance benchmarks and maximize investor flows. Both the best- and worst-performing funds increase portfolio volatility relative to their peers, as do those below their high-water marks. Funds with permissive redemption policies and those with concentrated ownership risk shift most aggressively. Laggard managers amplify volatility by increasing leverage and modifying asset class allocations, while top performers instead pursue contrarian strategies.