The Transition to Alternative Reference Rates in the OFR Financial Stress Index

Published: June 27, 2023

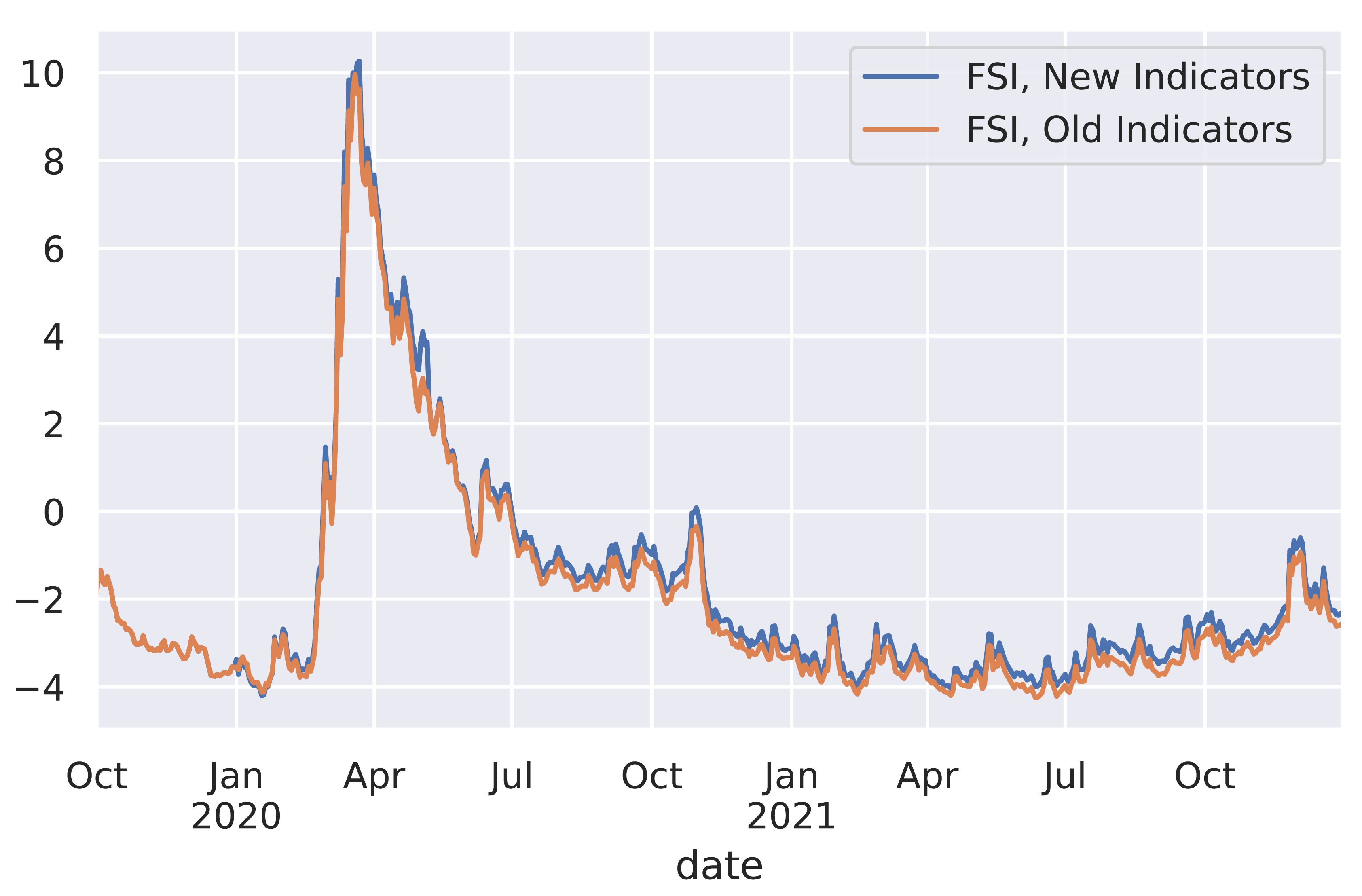

The OFR Financial Stress Index (OFR FSI or FSI) is a daily market-based snapshot of stress in global financial markets. Originally, the OFR FSI was constructed from 33 financial market variables that are correlated with some form of financial stress. Seven of these variables are based on LIBOR or other ceasing and/or already-ceased benchmark interest rates. As such, these seven variables are now obsolete. However, since its inception, the OFR FSI was intended to allow for the periodic replacement of obsolete variables as the need arises (Working Paper no. 23-07).

Abstract

The OFR Financial Stress Index (OFR FSI) is a daily market-based snapshot of stress in global financial markets that is constructed from 33 financial market variables. As of the time of writing, seven of these variables rely on obsolete reference rates. Since its inception, the OFR FSI was intended to allow for the periodic replacement of obsolete variables as the need arises. In this paper, I introduce replacements for these seven obsolete variables, and I make explicit the procedure with which the OFR FSI incorporates these new variables. Furthermore, I demonstrate generally that this replacement procedure produces an index with the following desirable properties: (1) the index is a weighted sum of the presently included variables; (2) removed variables no longer directly affect the index, and newly included variables do not modify historical values of the index; (3) the index uses all available historical data on the newly included variables to train the model; and (4) the volatility of the index is roughly comparable before and after the replacement.

Keywords: Financial Stability, Factor Model, Index Numbers

JEL Classifications: : C38, G01, C58, C55, C43